Natural Flavors Market Outlook

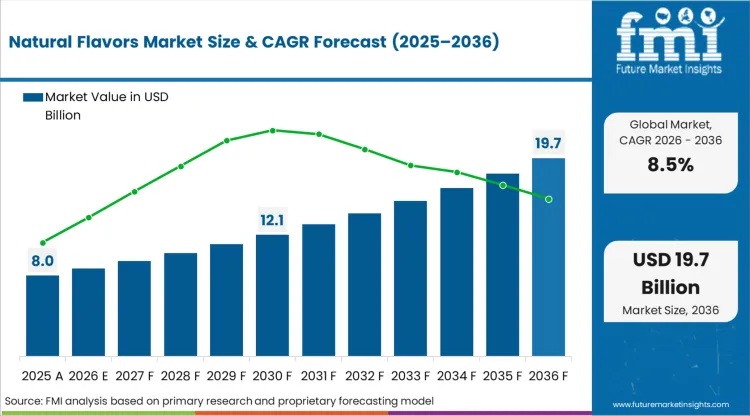

The global natural flavors market is entering a decade of structural transformation, driven by shifting consumer trust, regulatory scrutiny, and supply chain volatility. According to analysis by Future Market Insights (FMI), the market was valued at USD 8.0 billion in 2025 and is projected to reach USD 8.7 billion in 2026. By 2036, revenues are expected to climb to USD 19.7 billion, reflecting a robust CAGR of 8.5%.

This trajectory translates into an absolute dollar opportunity of USD 11.0 billion over ten years — a signal of fundamental change rather than incremental growth. The market is no longer expanding merely on rising consumption volumes. Instead, it is evolving as global food and beverage manufacturers recalibrate procurement strategies around label integrity, consumer trust, and supply security.

From Extraction to Precision: A Structural Pivot

The natural flavors sector is undergoing a technological shift. Traditionally reliant on direct botanical extraction, flavor houses are increasingly investing in precision fermentation and enzymatic processing. These technologies allow companies to stabilize volatile supply chains that are heavily exposed to climate disruptions affecting vanilla, citrus, cocoa, and other key crops.

Crop yield variability, driven by erratic rainfall patterns and rising temperatures, has intensified input price fluctuations. As a result, manufacturers are moving toward bio-based aromatics and controlled fermentation systems to reduce exposure to raw material shocks while maintaining “natural” classification compliance.

This pivot represents a supply-side hedge against agricultural instability — transforming natural flavors from a commodity-driven segment into a science-led innovation category.

Consumer Perception Driving Procurement Strategy

The demand engine behind this growth is increasingly data-led consumer psychology.

Recent behavioral insights show that 36% of consumers view “Labeled as Natural/Organic/Healthy” as a primary indicator of food safety. In a marketplace where ultra-processed foods face growing skepticism, the word “natural” has evolved from a marketing descriptor into a commercial gatekeeper.

For CPG manufacturers, natural certification is now:

· A prerequisite for premium shelf placement

· A competitive shield against clean-label challengers

· A long-term brand equity safeguard

This shift has forced legacy product portfolios to undergo reformulation cycles. Artificial synthetics are being phased out in favor of botanical extracts, essential oils, and fermentation-derived compounds — even when unit costs are higher.

Importantly, this is not an aesthetic transition. It is a risk-mitigation strategy designed to protect brand credibility in an era of declining consumer trust.

Absolute Dollar Growth Signals Premiumization

The projected USD 11.0 billion absolute growth reflects more than expanding consumption; it signals premiumization. Natural flavor ingredients command price premiums compared to artificial alternatives, particularly when sourced sustainably or certified organic.

As global middle-class populations expand across Asia-Pacific and Latin America, demand for “clean label” and minimally processed products is accelerating. Multinational beverage brands, dairy producers, and snack manufacturers are embedding natural flavor commitments into ESG disclosures and sustainability frameworks.

"Access the Industry Blueprint: Download Sample or Buy Full Analysis."

This institutionalization of natural sourcing strengthens long-term demand visibility.

Regulatory Pressure Reinforcing the Trend

Regulatory frameworks across North America and Europe are tightening around artificial additives. Clean-label transparency mandates and clearer ingredient disclosure requirements are increasing compliance risks for synthetic flavor usage.

Manufacturers are proactively transitioning portfolios before regulatory compulsion forces abrupt change. This forward-looking approach reduces reputational risk and enhances supply chain resilience.

As regulatory scrutiny intensifies, natural flavors increasingly function as a compliance insurance tool rather than merely a differentiation strategy.

Innovation Ecosystem Expanding

The innovation landscape is also broadening. Investments in biotechnology platforms are enabling:

· Yeast-based flavor biosynthesis

· Enzyme-assisted extraction techniques

· Waste-to-flavor circular economy models

These approaches improve yield efficiency while reducing land and water dependency. They also allow for consistent flavor profiles — a critical requirement for multinational brands operating across diverse markets.

By reducing reliance on geographically concentrated crops, biotechnology-backed production offers cost predictability and margin stabilization over time.

Competitive Outlook and Strategic Imperatives

Over the forecast period to 2036, competition within the natural flavors market is expected to intensify. Consolidation among flavor houses, strategic acquisitions of biotech startups, and long-term agricultural sourcing contracts will likely shape the competitive landscape.

Market participants focusing on the following pillars are positioned for leadership:

· Supply chain diversification

· Fermentation technology investment

· Transparent labeling compliance

· Sustainable sourcing certifications

The industry’s evolution underscores a broader truth: “natural” is no longer a niche positioning. It is becoming a structural baseline expectation.

Outlook: A Decade of Structural Realignment

With revenues expected to nearly double from USD 8.0 billion in 2025 to USD 19.7 billion by 2036, the natural flavors market is poised for sustained expansion. An 8.5% CAGR reflects not just growth, but recalibration across sourcing, processing, and branding strategies.

As climate volatility reshapes agricultural economics and consumer scrutiny intensifies, natural flavors are transitioning from optional enhancement to strategic necessity.

For manufacturers, the question is no longer whether to invest in natural flavor systems — but how quickly they can integrate innovation, ensure supply resilience, and secure consumer trust in an increasingly transparent food ecosystem.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware - 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com