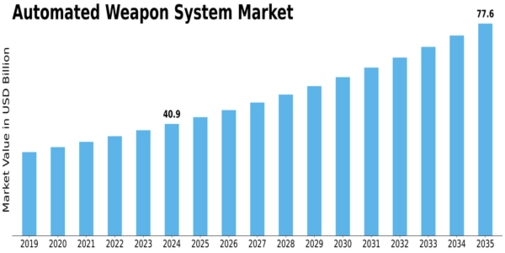

In the rapidly evolving domain of defence technology, the Automated Weapon System Market is being shaped by several global giants. According to MRFR, this market is estimated at USD 41.58 billion in 2024 and projected to hit USD 77.64 billion by 2035, growing at a CAGR of 5.84 %.

Industry Overview

Automated weapons—including unmanned platforms, robotics, advanced sensors, and integrated command systems—are increasingly central to modern military doctrine. Firms that can deliver end-to-end autonomous solutions, or integrate effectively into networked defence systems, are at an advantage. MRFR highlights that integration of AI and machine learning (ML) is a key differentiator.

Market Outlook

A steady but durable growth trajectory suggests that the opportunity lies in long-term contracts, legacy upgrade cycles and global defence modernisation. The predicted nearly USD 77.64 billion size by 2035 underscores the scale of investment being channelled.

Key Players & Competitive Landscape

According to MRFR, the major players include:

- Lockheed Martin Corporation (US)

- Northrop Grumman Corporation (US)

- Raytheon Technologies Corporation (US)

- BAE Systems PLC (UK)

- General Dynamics Corporation (US)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Elbit Systems Ltd. (Israel)

- Saab AB (Sweden)

These companies are pursuing various strategies such as:

- Mergers & acquisitions to expand defence-automation portfolios

- Strategic partnerships with governments or other defence firms

- Heavy R&D investment into AI, sensors, robotics and unmanned platforms

- Geographic expansion into high-growth regions (e.g., Asia-Pacific)

Impact of Key Players on Market Growth

The presence of these major firms contributes to:

- Faster adoption of advanced automated weapon systems due to their credibility and scale

- Standardisation of modular-system offerings that can be adapted globally

- Price competition and innovation diffusion as smaller players adopt similar technologies

Additionally, as these players expand globally, they influence procurement patterns and help push the market overall.

Segmentation Growth in Relation to Key Players

Major players are well-positioned in dominant segments: land systems, command & control components, on-premises deployment. At the same time, they are also moving into faster‐growing segments: aerial systems, sensor subsystems, cloud‐based models. This dual-track strategy ensures they benefit from both current dominance and future growth pockets.

Outlook for Emerging Players

While the big players dominate now, there is nevertheless space for niche innovators—especially in sensors, AI/ML for automation, unmanned aerial systems and cloud integration. New entrants or smaller specialist firms that partner with established contractors may find growth opportunities as the overall market size expands.

Final Thoughts

As the automated weapon system market forecast approaches nearly USD 77.64 billion by 2035, major defence contractors will remain the backbone of this segment. Their strategic investments, partnerships and technology road-maps will shape how the market evolves. For companies in adjacent technology domains (AI, robotics, sensors) the key is to align with these major players or carve out differentiated solutions that address high‐growth segments.

Related Report:

Armored Vehicles Upgrade and Retrofit Market

Commercial Aircraft Windows and Windshield Market

Military Electro-Optical and Infrared Systems Market